税制改正の重要ポイント

2025年(令和7年)は、年の中途で亡くなられた方の所得税申告、すなわち「準確定申告」においても影響があるため注意が必要です。

税制改正の主な内容(令和7年度)

- 基礎控除額の引き上げ:従来の48万円から所得金額によっては最大95万円へ

- 給与所得控除の最低保障額:55万円 → 65万円

- 特定親族特別控除の創設:19歳以上23歳未満で所得が123万円以下の扶養親族がいる場合の特別控除

- 施行日:2025年12月1日

これら基礎控除等の改正内容は、施行日である12月1日から実務として運用スタートするため、準確定申告の場合には、その「申告日」が12月1日以降であるか否かにより、控除額が異なるケースがあります。

準確定申告で注意すべき点

準確定申告は通常の確定申告とは異なります。通常その年の1月から12月までの12か月分の所得について確定申告を行うところ、例えば「年の中途で死亡した場合」の他、納税管理人を設置せずに海外転勤等のため1年以上の予定で「年の中途で出国をする場合」について、申告対象期間をその事由の生じた日で一旦区切った上で申告を行う、という点です。

年の中途で相続が発生した場合、被相続人(亡くなられた方)の1月1日から死亡日までの期間に区切って、確定申告を行うこととなります。これが、「準確定申告」となり、申告・納税義務者となる相続人は、相続を知った日の翌日から4ヶ月以内に申告を行うこととなります。

➤相続が発生した場合の準確定申告期限

①2025年3月10日に相続が発生した場合⇒2025年7月10日までに準確定申告を行います。

②2025年8月10日に相続が発生した場合⇒2026年12月10日までに準確定申告を行います。

この際、以下のようなケースが発生します:

- 11月30日以前に申告した場合(①のケース):改正後の控除額は適用されていません

- 12月1日以降に申告した場合(②で12/1以降に提出):改正後の控除額が適用されています

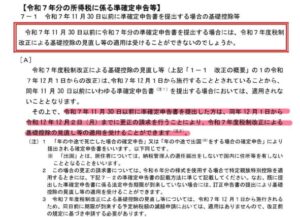

今回の税制改正の「施行日」よりも前に申告を行っていた場合には、現状改正後の控除額は適用されていません。しかし、準確定申告のようにイレギュラーな事象が年の中途に発生した場合であっても、令和7年中の所得であることに変わりありません。そこで、11月30日以前に既に準確定申告を済ませてしまった場合でも、令和7年中の所得に関する申告については、改正後の控除額適用のため、「更正の請求」による救済策を検討する余地があるということになります(国税庁|令和7年度税制改正(基礎控除の見直し等関係)Q&A7-1)。

更正の請求とは?

更正の請求とは、既に提出した申告内容を修正して納めすぎた税金を還付する手続きです。令和7年分の所得について行った準確定申告については、控除の適用可否を再検討することも念頭に入れて置く必要があります。

しかし、相続税の申告期限との兼ね合いを考慮すると、還付税額や還付加算金がいつ頃確定するのかについては断定できません。このため、相続税の申告期限や金額の影響度合い等を考慮の上で、最適解を見つけることが求められる場面もでてくるのではないかと考えます。はじめから還付申告ということが分かっているケースにおいては、申告期限が11月30日以前に到来していても、あえて12月1日以降に申告書を提出して一度で完結させるという策を講じる場合もあるでしょう。

令和7年分準確定申告のポイント

- 申告日が2025年12月1日以降なら、改正後の控除額を適用

- 11月30日以前に申告した令和7年分準確定申告は、控除額が旧制度のまま → 更正の請求を行う効果を検討しましょう

Key Points of the 2025 Tax Reform

In 2025 (Reiwa 7), special attention is also required when filing a “quasi-final tax return” (jun-kakutei shinkoku) for individuals who passed away during the year. This is because the amount of applicable income deductions may vary depending on the filing date.

Main Highlights of the 2025 Tax Reform

- Increase in Basic Deduction: Raised from the standard ¥480,000 to a maximum of ¥950,000 depending on income level

- Minimum Salary Income Deduction: Increased from ¥550,000 to ¥650,000

- New Special Deduction for Certain Dependents: Applies when the taxpayer has a dependent aged 19–22 with income of ¥1.23 million or less

- Effective Date: December 1, 2025

Since these changes take effect from December 1, 2025, the filing date of a quasi-final return determines whether the revised deduction amounts apply. Returns filed on or after December 1 may be eligible for the new deductions, while those filed earlier may not.

Important Notes on Quasi-Final Tax Returns

Unlike regular final tax returns, which cover income from January 1 to December 31, a quasi-final return is required when a taxpayer:

- Passes away during the year, or

- Departs Japan mid-year for an overseas assignment of one year or more without appointing a tax agent.

In such cases, the taxable period is cut off at the date of death or departure, and a quasi-final return must be filed accordingly.

For example, if a person passes away mid-year, the return must cover the period from January 1 to the date of death. The legal heirs, who become responsible for filing and paying the taxes, must submit the return within four months from the day they became aware of the inheritance.

➤ Filing Deadlines for Quasi-Final Returns in Case of Inheritance

- If the individual passed away on March 10, 2025 → File by July 10, 2025

- If the individual passed away on August 10, 2025 → File by December 10, 2025

Implications of Filing Timing

- Filed before November 30 (e.g., Case ①): Revised deduction amounts do not apply

- Filed on or after December 1 (e.g., Case ②): Revised deduction amounts do apply

Even if a quasi-final return is filed before the reform’s effective date, the income still pertains to the 2025 tax year. Therefore, a corrective claim (kōsei no seikyū) may be considered to apply the revised deductions retroactively.

What Is a Request for Correction?

A request for correction is a procedure to amend a previously filed return and request a refund for overpaid taxes. For quasi-final returns related to 2025 income, taxpayers should consider whether the revised deductions can be applied retroactively.

However, due to the interaction with the inheritance tax filing deadline, it may be difficult to determine exactly when the refund or interest will be finalized. In such cases, it is important to weigh the impact of inheritance tax deadlines and refund amounts to determine the best course of action.

In situations where a refund is expected from the outset, some may choose to intentionally file the return after December 1, even if the original deadline falls before that date, in order to benefit from the revised deductions in a single filing.

Summary

- If the filing date is on or after December 1, 2025, the revised deduction amounts apply

- If a quasi-final return for 2025 was filed before November 30, the old deduction amounts apply → Consider filing a request for correction to apply the revised deductions