「相続税は日本の税収の内、どのぐらいの割合を占めるのでしょうか?」

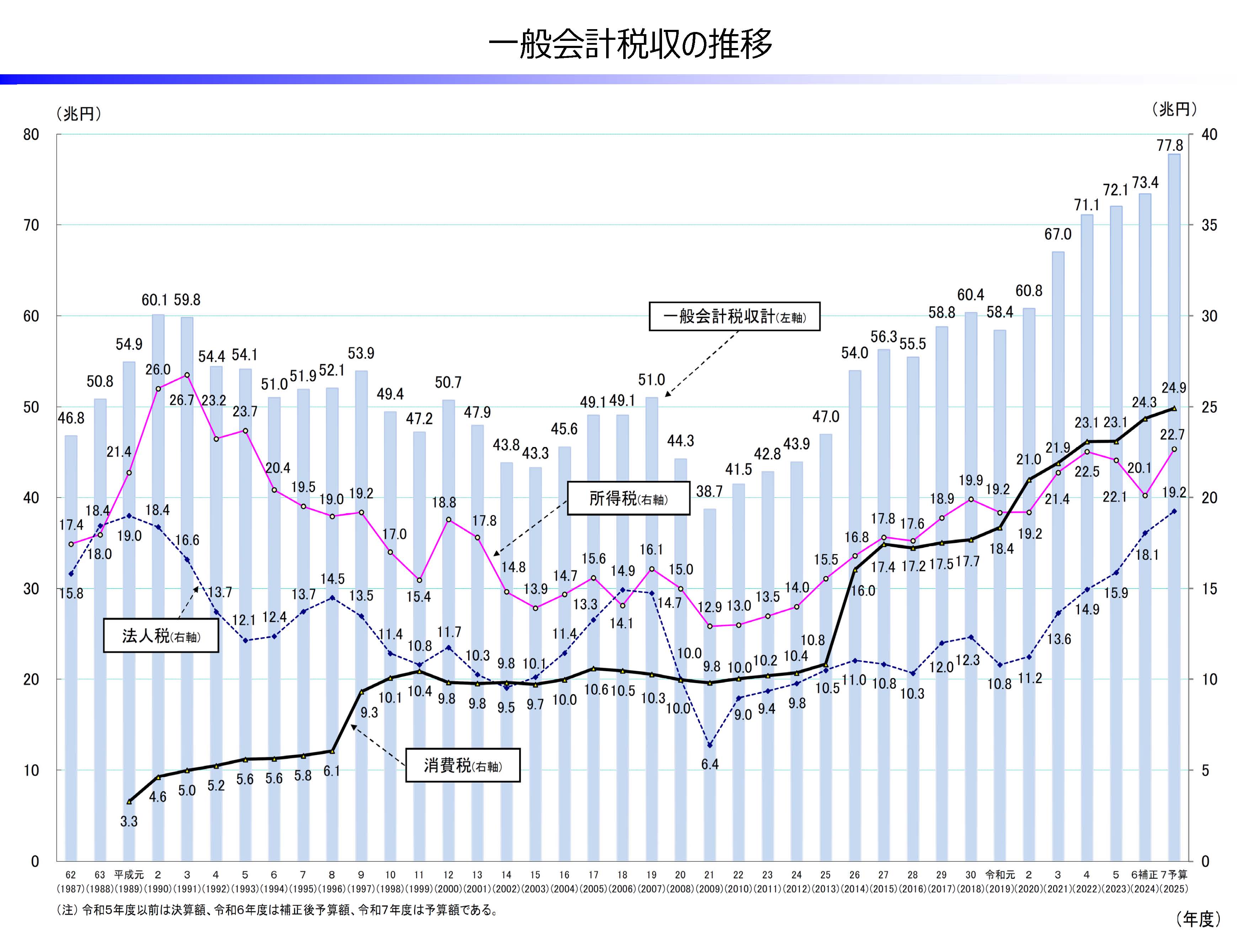

日本の税収は、令和6年度(2024年度)に5年連続で過去最高を更新しました。

これは、以下のグラフの通り一般会計税収推移が、ここ数年継続して右肩上がりとなっていることから一目瞭然です。

※出典:税収に関する資料 : 財務省

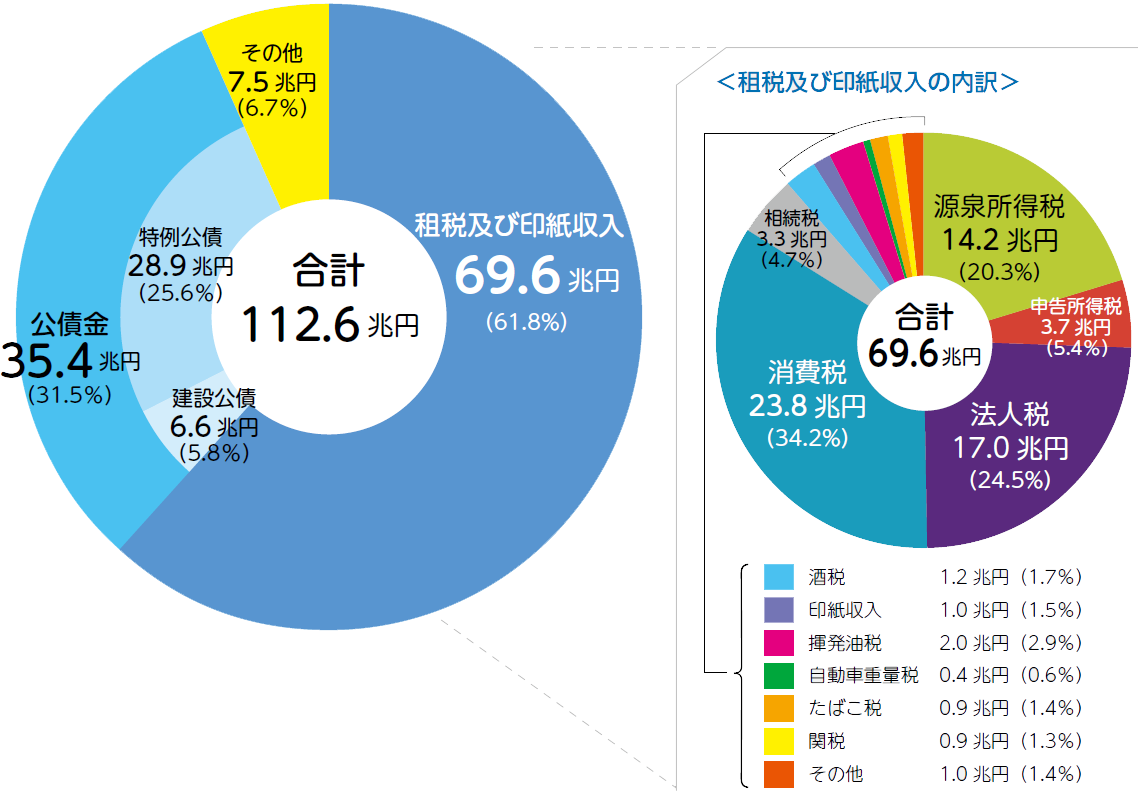

以下は、国税庁資料による、令和6年度当初予算からの各税目の含有比率ですが、令和6年度の歳入約112兆円の内、租税収入が約6割強の69兆円として、この内相続税の占める割合は、たったの4.7%(3.3兆円)でした。それでも、租税収入の増加傾向は、消費税・所得税・法人税の堅調な推移によるものです。

国の収入(令和6(2024)年度一般会計歳入(当初予算))

※1 公債金は、公共事業費などを賄うために発行された建設公債と歳入の不足を埋め合わせるために発行された特例公債による収入であり、全てが将来返さなければならない借金です。

※出典:Ⅰ 国税庁について|国税庁

相続税の割合が低い理由

相続税の税収割合が低い背景には、以下のような要因があります:

- 課税対象者が限られている:相続税が課されるのは、死亡者のうち約8〜9%程度。10人に1人という割合です。消費税・所得税・法人税とは異なり、保有する財産に限定され、死亡時に一度限り課税。

- 基礎控除の存在:3,000万円+600万円×法定相続人の控除があるため、非課税となるケースが多い。

- 不動産価格の地域格差:地方では地価が低く、課税対象となる資産が少ない傾向。

それでもなぜ相続税は注目されるのか?

割合が小さいにもかかわらず、相続税が注目される理由は以下の通りです:

- 都市部に影響:都市部では不動産評価額が高く、自宅のみでも基礎控除を上回る可能性あり

- 基礎控除の効果:基礎控除が平成27年(2015年)から減少したことに伴い申告対象となる裾野が広がり、資産防衛のため関心が高まっている。

- 納税資金の準備が必要:現金以外の資産(不動産など)が多い場合、納税に苦慮するケースも。

まとめ

相続税は国税収入全体からすると約4.7%と、割合としては小さいですが、個人にとっては大きな負担となる可能性があるため、早めの対策をお勧めいたします。

What share of total tax revenue does inheritance tax represent?

“How much of Japan’s national tax revenue comes from inheritance tax?”

Japan’s tax revenue reached a record high for the fifth consecutive year in FY2024 (Reiwa 6).

As shown in the above chart, the trend of general account tax revenue has been steadily rising in recent years.

Source: Tax Revenue Data – Ministry of Finance税収に関する資料 : 財務省

According to materials from the National Tax Agency, the initial budget for FY2024 shows that out of total government revenue of approximately ¥112 trillion, tax revenue accounts for just over 60%, or about ¥69 trillion.

Of this, inheritance tax makes up only 4.7% (¥3.3 trillion).

The continued growth in tax revenue is largely driven by steady increases in consumption tax, income tax, and corporate tax.

Source: “About the National Tax Agency” – National Tax AgencyⅠ 国税庁について|国税庁

Why Is the Share of Inheritance Tax So Low?

Several factors contribute to the relatively small share of inheritance tax in total tax revenue:

- Limited number of taxpayers: Inheritance tax applies to only about 8–9% of all deaths—roughly 1 in 10 people. Unlike consumption, income, or corporate taxes, it is levied only once at the time of death and only on owned assets.

- Basic exemption: Many inheritances are tax-free due to the exemption formula: ¥30 million + ¥6 million × number of statutory heirs.

- Regional disparities in property values: In rural areas, land prices tend to be lower, resulting in fewer taxable assets.

Why Does Inheritance Tax Still Attract Attention?

Despite its small share, inheritance tax remains a topic of concern for several reasons:

- Impact in urban areas: High property values in cities mean that even a single home can exceed the basic exemption threshold.

- Reduced exemption since 2015: The narrowing of the basic exemption in 2015 (Heisei 27) expanded the range of people required to file, increasing public interest in asset protection.

- Need for liquidity: When assets are primarily non-cash (e.g., real estate), preparing funds for tax payment can be challenging.

Conclusion

Inheritance tax accounts for approximately 4.7% of total national tax revenue—a relatively small proportion.

However, for individuals, the financial burden can be significant.

Early planning and consultation are strongly recommended.