相続と健康寿命の交差点で

「人生100年時代」、本当でしょうか?

確かに、日本の「平均寿命」は年々延び続けており、実際100歳代の相続は徐々に珍しくなくなっているという実感はあります。

しかし、税務の現場で相続に関わるたびに、私はこの数字の裏にある“もうひとつの寿命”に思いを馳せます。それが「健康寿命」です。

平均寿命と健康寿命のギャップがもたらす課題

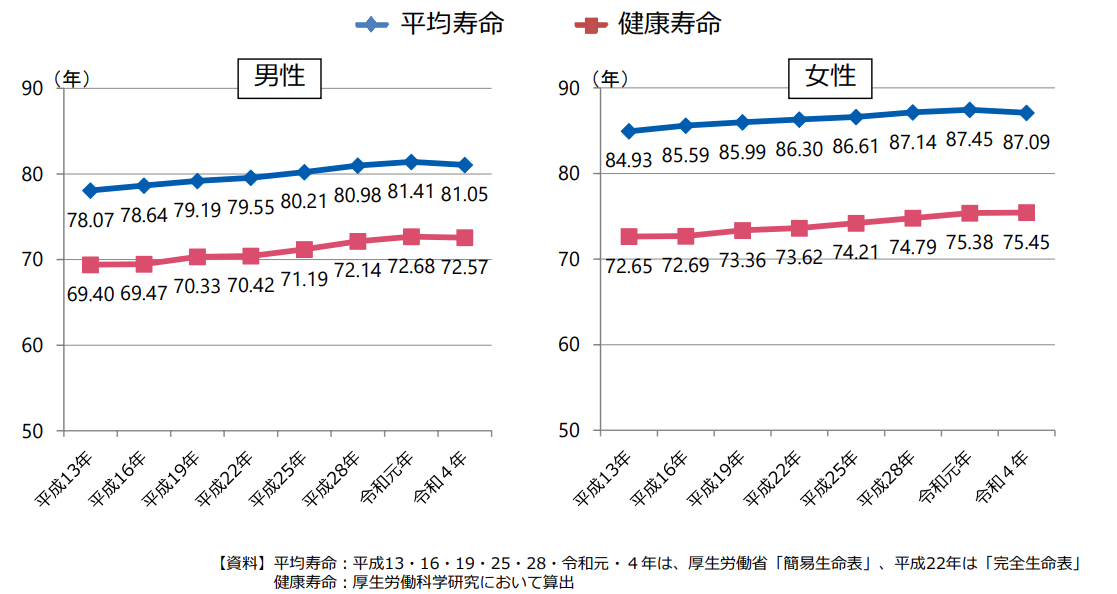

日本では2024年(令和6年)厚生労働省のデータより、平均寿命は男性81歳、女性87歳と延びる一方で、健康寿命は男性72歳、女性75歳と、認知症や寝たきりなどにより「自分らしく生きられる期間」が短くなる傾向があります(出典:厚生労働省life24-02.pdf、健康日本21アクション支援システム Webサイト)。このギャップは、相続の現場にも影響を及ぼします。

相続税の申告に携わる中で、意思能力を失ったまま財産の整理が進められるケースや、介護費用が相続財産に大きく影響する場面に直面することも少なくありません。

「長生き=幸せ」とは限らない。

だからこそ、健康寿命を意識した人生設計と、相続への備えは切り離せないテーマなのです。

- 本人の意思確認ができないまま遺産分割が進むケース

- 成年後見制度の利用による手続きの複雑化

- 長期の介護費用が財産を圧迫し、相続税の納税資金に影響することも

出典:一般社団法人高齢者住宅協会

出典:一般社団法人高齢者住宅協会

健康寿命を意識した相続対策のすすめ

こうした課題に備えるための対策として

- 財産の棚卸しと相続税のシミュレーション:相続税が発生する可能性の有無、相続税が発生する場合にどのような事前対策が考えられるのかを自分自身で事前に検討することが可能です。

- 遺言書の作成:公正証書遺言、自筆証書遺言、秘密証書遺言など遺言書の作成方法は様々です。

- 家族信託の活用:ここ最近認知症を意識して財産管理の一手段として検討されています。

元気なうちにこそ、未来を描く

たとえ寿命が延びても、その期間が全て健康とは限りません。不老不死の動物はいませんので、通常何も意識せずに過ごしていれば歩行能力等の身体能力の衰えと共に、意思能力も衰えていくのが自然な現象です。

まだまだ大丈夫、と健康状態を過信するのではなく、どうすれば健康寿命をより長く、そして前向きな気持ちで人生を全うすることができるのか、年齢を問わず自分自身と家族を大切に生きる意味でも、まずは日々の生活習慣の見直しと、健康に対する意識改革からはじめましょう!

At the Intersection of Inheritance and Healthy Life Expectancy

Is the “100-Year Life” Really Within Reach?

It’s true that Japan’s average life expectancy continues to rise year after year. In fact, inheritances involving centenarians are gradually becoming less of a rarity.

However, every time I encounter an inheritance case in my tax practice, I’m reminded of another kind of lifespan that lies behind the numbers: healthy life expectancy.

The Challenges Created by the Gap Between Average and Healthy Life Expectancy

According to data from Japan’s Ministry of Health, Labour and Welfare in 2024 (Reiwa 6), while the average life expectancy has risen to 81 years for men and 87 years for women, healthy life expectancy remains shorter—72 years for men and 75 years for women—indicating a growing trend in which the period of life one can live with independence and dignity is being shortened by conditions such as dementia or being bedridden. (Source: Ministry of Health, Labour and Welfare “life24-02.pdf”; Health Japan 21 Action Support System website).This gap has real implications for inheritance.

In my work preparing inheritance tax filings, I often encounter situations where assets must be organized even though the individual has lost decision-making capacity, or where long-term care expenses significantly reduce the estate’s value.

Longevity does not always equal happiness.

That’s why life planning that takes healthy life expectancy into account—and preparing for inheritance—are inseparable themes.

Common challenges include:

- Asset division proceeding without the individual’s clear intent

- Complex procedures due to the use of adult guardianship systems

- Long-term care costs straining the estate and affecting funds available for inheritance tax payment

Inheritance Planning with Healthy Life Expectancy in Mind

To prepare for these challenges, consider the following strategies:

- Personal Asset Review and simulate inheritance tax: First, assess whether inheritance tax is likely to apply. If so, explore what preemptive measures can be taken.

- Prepare a will: There are several formats, including notarial wills, handwritten wills, and sealed wills.

- Utilize family trusts: Increasingly considered as a way to manage assets in anticipation of dementia or declining capacity.

Envisioning the Future While You’re Still Well

Even if life expectancy increases, that doesn’t guarantee those extra years will be healthy. No living creature is immortal. Without conscious effort, it’s natural for both physical and cognitive abilities—like walking or decision-making—to decline over time.

Rather than assuming “I’m still fine,” we should ask: How can I extend my healthy years and live with a positive spirit?

No matter our age, living with care—for ourselves and for our families—starts with two essential steps: reexamining our daily habits and reshaping our mindset toward health.